NJ Health Insurance Coverage Guide: 2026 Practical Tips

TL;DR:

- Health insurance coverage in New Jersey varies by plan type, network rules, and coverage details.

- Understanding plan differences and costs helps choose the most suitable coverage and avoid surprises.

- Local providers like Garden State Medical Group assist patients in navigating insurance and access to care.

Two people can have the same job, live in the same town, and both carry health insurance cards, yet one pays $20 for a specialist visit while the other owes $400 out of pocket. That gap is not random. It comes down to plan type, network rules, and how New Jersey’s specific insurance landscape shapes what’s actually covered. Health insurance coverage in New Jersey comes in multiple forms, each with different rules and protections. This guide breaks down the major options, how costs work, and what you can do right now to make smarter decisions about your care.

Table of Contents

- How health insurance coverage works in New Jersey

- Types of health insurance plans and how they’re different

- Understanding costs: Premiums, deductibles, and financial help

- Medicaid, special cases, and why some New Jerseyans remain uninsured

- A local expert’s perspective: What really matters in New Jersey health insurance coverage

- How Garden State Medical Group supports your coverage journey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Coverage goes beyond a card | Having health insurance in New Jersey means knowing what services, costs, and rules apply to your plan. |

| Multiple options available | Employer, marketplace, Medicaid, and Medicare plans each serve different groups and needs. |

| Costs are manageable with help | Most New Jerseyans qualify for subsidies that lower premiums and out-of-pocket costs significantly. |

| Special cases require attention | Life changes and lower income open up alternatives and year-round enrollment opportunities. |

| Provider access matters | Choosing the right plan type affects how easily you can see doctors and access care locally. |

How health insurance coverage works in New Jersey

When people say they’re “covered,” they usually mean a health plan will pay some portion of their medical bills. But that’s where simplicity ends. Whether your plan covers a specific doctor, drug, or procedure depends entirely on the details buried in your policy documents.

Coverage expectations in New Jersey include access to preventive care, emergency services, prescription drugs, and mental health treatment. Still, gaps in coverage can leave you with unexpectedly high bills if you see an out-of-network provider or miss a prior authorization requirement.

In New Jersey, coverage primarily comes through employer-sponsored plans, the ACA marketplace called GetCoveredNJ, NJ FamilyCare (which includes Medicaid and CHIP), and Medicare. Each pathway has its own rules, costs, and benefits. Your primary care options will often depend on which program you’re enrolled in.

New Jersey also has a state individual mandate. This means nearly all adults are required to have qualifying health coverage or pay a state tax penalty when they file. There is no federal penalty anymore, but the New Jersey penalty is real and based on your income and family size.

Here is a quick look at the main coverage sources available in New Jersey:

- Employer-sponsored insurance: Offered through your job, often with shared premium costs

- GetCoveredNJ (ACA Marketplace): For individuals and families buying their own coverage

- NJ FamilyCare: Free or low-cost coverage for qualifying low-income residents

- Medicare: Federal program for adults 65 and older, or those with qualifying disabilities

Knowing which program you qualify for is just the first step. Knowing what that program actually covers in practice is where the real work begins.

You can also review the accepted insurance plans at local providers before choosing a plan to confirm your preferred doctors are in-network.

Types of health insurance plans and how they’re different

With the basics established, let’s compare the specific health plan types you’ll encounter when shopping for coverage in New Jersey.

The four most common plan structures are HMO, PPO, EPO, and Medicaid or Medicare. Each has a distinct approach to networks and referrals, and that difference shapes both your costs and your convenience.

Plan types and networks determine which doctors and hospitals you can use without paying extra. Here’s how they compare:

| Plan Type | Requires Referrals? | Out-of-Network Covered? | Typical Cost Level |

|---|---|---|---|

| HMO | Yes | No | Lowest |

| PPO | No | Yes (higher cost) | Higher |

| EPO | No | No | Moderate |

| Medicaid (NJ FamilyCare) | Sometimes | Limited | Lowest/Free |

| Medicare | Varies by plan | Varies | Moderate |

An HMO, or Health Maintenance Organization, requires you to choose a primary care physician who coordinates all your care. You need a referral before seeing a specialist. The tradeoff is that premiums and copays are usually the lowest available.

A PPO, or Preferred Provider Organization, gives you more freedom. You can see specialists without a referral and even go outside the network, though you’ll pay more for that flexibility. PPO premiums tend to be higher.

An EPO, or Exclusive Provider Organization, sits in between. No referrals needed, but you’re limited strictly to in-network providers. Go outside the network and you pay the full bill yourself.

The referral requirements and network rules for each plan type are also tied to metal levels: Bronze, Silver, Gold, and Platinum. Bronze plans carry lower premiums but higher out-of-pocket costs when you need care. Platinum plans flip that equation.

Pro Tip: If you have a specialist you already see regularly, check whether they accept your target plan’s network before enrolling. Switching plans mid-treatment can be disruptive and expensive.

Understanding costs: Premiums, deductibles, and financial help

Now that you know the options, the next crucial piece is understanding what you’ll pay, and how to get help.

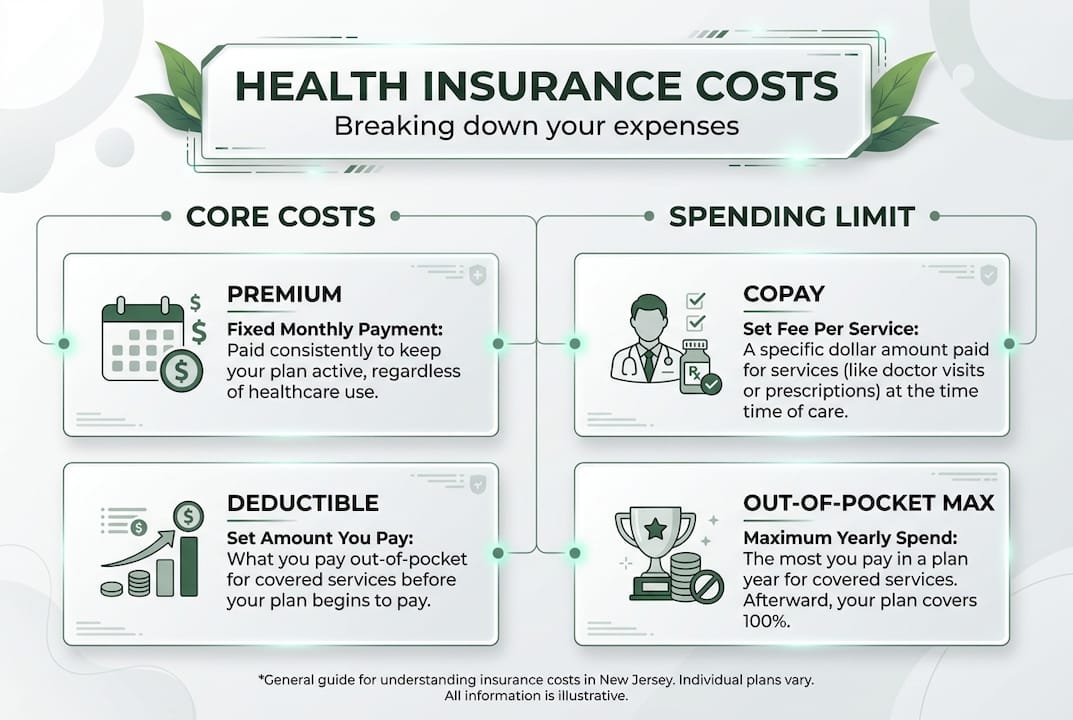

Health insurance costs involve several moving parts, and each one affects your actual spending in a different way.

Premium is the monthly amount you pay just to keep your plan active, whether or not you use any medical services that month. Deductible is the dollar amount you must pay for covered services before your insurance starts sharing costs. Copayment is a fixed fee you pay per visit or service, like $30 for a primary care appointment. Coinsurance is your percentage share of costs after meeting your deductible, such as paying 20% while insurance pays 80%.

The out-of-pocket maximum is your financial safety net. Once you hit that ceiling in a plan year, your insurance covers 100% of covered costs for the rest of the year.

Financial help is more available than many people realize. 9 in 10 New Jerseyans who enroll through GetCoveredNJ qualify for assistance, with average financial help reaching $589 per month per person. Nearly half pay $10 or less per month for their plan after subsidies.

Here’s a summary of what each cost term means in practice:

- Premium: Paid monthly, keeps your coverage active

- Deductible: You pay this first before insurance helps with most services

- Copay/Coinsurance: Your share each time you receive care

- Out-of-pocket maximum: Your yearly cost ceiling

Before enrolling, checking your coverage for specific services can save you from surprise bills. You can also explore how medical services work at local practices to understand what’s typically billed and how insurance applies.

Pro Tip: If you’re generally healthy and rarely need care, a Bronze plan with lower premiums may save you money. If you manage a chronic condition, a Gold or Platinum plan could cost less overall once you factor in your regular medical expenses. Learn more about planning around preventive services to maximize your benefits.

Medicaid, special cases, and why some New Jerseyans remain uninsured

Coverage rules can become complicated, especially for low-income adults, people in transition, and special situations.

NJ FamilyCare is New Jersey’s Medicaid and CHIP program. Eligibility extends up to 138% of the federal poverty level, which equals roughly $1,800 per month for a single adult. There is no asset test, and enrollment is available year-round. Coverage includes doctor visits, hospital care, prescription drugs, and behavioral health services.

But not everyone who qualifies actually enrolls, and not everyone qualifies. Here are four common situations where coverage access gets complicated:

- Job loss or change: Losing employer coverage triggers a Special Enrollment Period, giving you 60 days to sign up for a new plan through GetCoveredNJ or NJ FamilyCare.

- Marriage or new dependent: A qualifying life event opens a window to adjust your coverage outside of Open Enrollment.

- Moving to New Jersey: Relocating to a new coverage area qualifies you for a Special Enrollment Period.

- Income change: If your income drops significantly, you may gain Medicaid eligibility even outside enrollment periods.

Special Enrollment Periods are time-sensitive, so acting quickly after a life event matters. Missing the window could leave you uninsured for months.

Despite these options, the uninsured rate in NJ rose to 7.7% in 2024, driven primarily by coverage loss after the pandemic-era continuous enrollment protections ended. Many of those who lost coverage were low-income adults who fell through gaps between Medicaid and marketplace eligibility.

For people managing ongoing conditions, staying enrolled is especially critical. Resources around chronic care management and Medicare options in NJ can help you understand your longer-term coverage path. You can also explore programs for special circumstances at local practices that serve patients navigating coverage transitions.

A local expert’s perspective: What really matters in New Jersey health insurance coverage

After working with patients across North Bergen and Secaucus, one thing becomes clear: having a health insurance card does not automatically mean you have access to the care you need.

Network restrictions are the biggest hidden barrier. A plan may appear affordable until you discover your regular doctor is out-of-network, or that a needed specialist requires a referral you weren’t aware of. Insurer practices like downcoding, where a provider’s billing code is changed to a less complex one, can also shift unexpected costs to patients after the fact.

The most common mistake we see is people assuming their coverage will work the same way it always has, year after year. Plans change annually. Formularies (the list of covered drugs) change. Networks shift. A provider that was in-network last year may not be this year.

Our honest advice is to review your plan every year during Open Enrollment, not just when something goes wrong. Ask your provider questions, check the drug list, and confirm network status for every specialist you see. Understanding your primary care choices and how they interact with your plan type is a practical first step that many people overlook until it’s too late.

How Garden State Medical Group supports your coverage journey

If you’re ready to take action, local providers can help you bridge the gap between what’s “covered” and what’s actually accessible. Understanding your plan is one thing. Finding a practice that works with it is another.

At Garden State Medical Group, we accept a wide range of insurance plans and work with patients to make the most of their coverage. Whether you need primary care services, diagnostic and radiology services, or support through one of our special programs for conditions like diabetes, bone health, or weight management, we’re here to make healthcare in North Bergen and Secaucus more accessible. Contact our office today to discuss your coverage and schedule an appointment that fits your needs.

Frequently asked questions

What is the difference between an HMO and a PPO plan in New Jersey?

HMO plans require you to use a specific network of doctors and get referrals for specialists, while PPO plans offer greater provider choice, allow out-of-network care at a higher cost, and do not require referrals.

Can I get health insurance in New Jersey outside of Open Enrollment?

Yes, you may qualify for a Special Enrollment Period if you experience a major life event. Life events such as job loss, marriage, or moving to a new area all trigger enrollment opportunities.

How do New Jersey subsidies make health insurance more affordable?

State and federal subsidies work together to reduce your monthly premium significantly. Nearly half of enrollees pay $10 or less per month after financial help is applied.

Who qualifies for NJ FamilyCare, and what does it cover?

Adults earning up to 138% of the federal poverty level are eligible, and coverage includes doctor visits, hospital care, and prescriptions with no asset test required.

What happens if I don’t have health insurance in New Jersey?

You may owe a state tax penalty unless you qualify for an exemption under New Jersey’s individual insurance mandate, which remains in effect for 2026.