Insurance & NJ Healthcare Access: What You Need to Know

TL;DR:

- Insurance in New Jersey often does not guarantee affordable or timely primary care access.

- Plan type, network restrictions, and high deductibles significantly impact healthcare costs and choices.

- Improving insurance literacy helps patients navigate barriers and utilize their coverage effectively.

Having health insurance in New Jersey is an important step toward getting care. But it does not automatically open every door. Even insured adults in New Jersey can face barriers like high out-of-pocket costs, network gaps, and confusing plan rules that make routine primary care harder to reach than expected. As Rutgers Policy Lab research highlights, affordability and insurance design can still block access to routine primary care even for covered individuals. This guide breaks down how insurance actually works in real life, what it guarantees and what it does not, and practical steps you can take to use your plan effectively.

Table of Contents

- The basics: What health insurance does (and doesn’t) guarantee in New Jersey

- How insurance design impacts your costs and choices

- The big picture: Primary care spending and policy in New Jersey

- Insurance literacy: Why understanding your plan matters as much as having one

- A critical view: When insurance design creates barriers instead of solutions

- Our perspective: What New Jersey adults need to know about insurance and primary care

- Connect with trusted primary care in New Jersey

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Coverage isn’t enough | Insurance does not automatically guarantee affordable or easy access to primary care in New Jersey. |

| Plan design shapes access | Your costs and ability to see a provider depend on plan type, network rules, and coverage details. |

| State investment matters | How much New Jersey spends on primary care affects the availability and quality of services you can get. |

| Insurance literacy is crucial | Understanding your plan prevents mistakes, high bills, and missed care opportunities. |

| Watch for design pitfalls | Even with insurance, high deductibles or complex processes can still limit protection from big costs. |

The basics: What health insurance does (and doesn’t) guarantee in New Jersey

Many people in New Jersey assume that having an insurance card means they can see any doctor, anytime, at a low cost. The reality is more layered than that. Your insurance plan sets the rules for which doctors you can see, how much you pay for services, and which treatments require advance approval. Understanding those rules is the first step to getting the most from your coverage.

Insurance covers certain services, but it does not cover everything at the same rate. Preventive visits might be free under your plan, while specialist visits come with a copay or a deductible you must first meet. A deductible is the amount you pay out of pocket before your insurance starts sharing costs. Once you reach your deductible, you typically pay coinsurance, which is a percentage of the bill, until you hit your annual out-of-pocket maximum.

Provider networks are another major factor. Most plans require you to use doctors and facilities within their network to receive full benefits. If you see an out-of-network provider, you may pay significantly more or receive no coverage at all. Rutgers Policy Lab findings note that for many people, coverage doesn’t guarantee they can afford care, find a provider, or even get an appointment.

Before you book any appointment, it is worth taking the time to check insurance coverage details for your specific plan. You can also review accepted insurance plans at practices like Garden State Medical Group to make sure your provider is in-network before you show up.

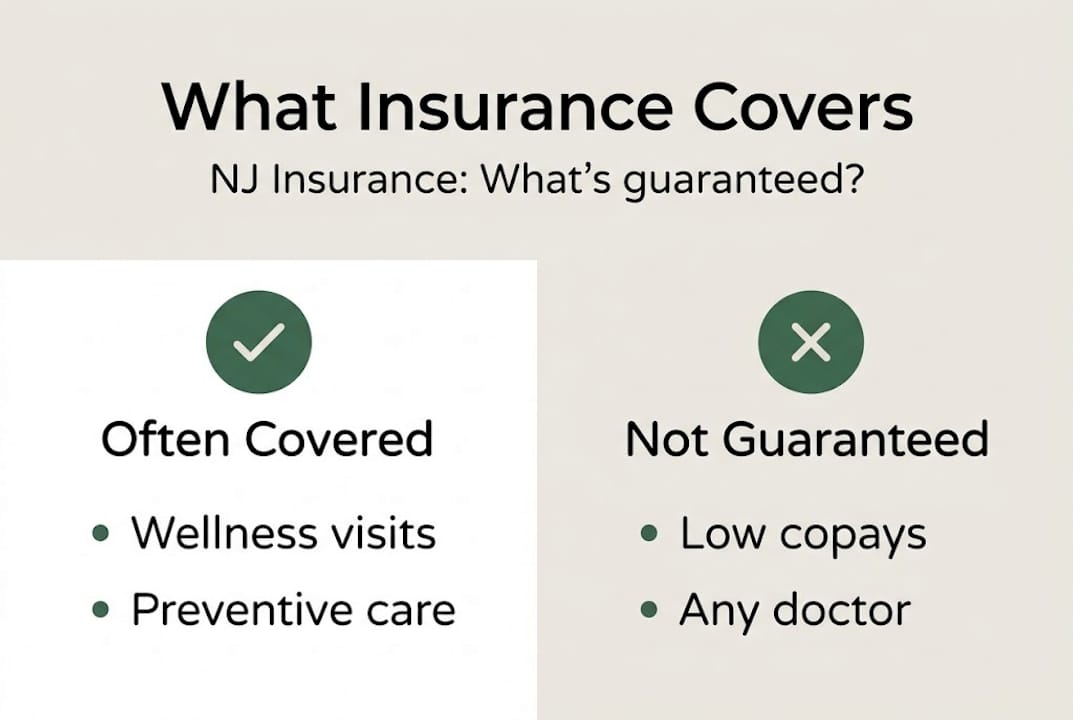

Here is a quick look at what insurance typically does and does not cover automatically:

| What insurance often covers | What it may NOT guarantee |

|---|---|

| Annual wellness visits (often free) | Appointment availability |

| Emergency care | Affordable specialist access |

| Preventive screenings | Out-of-network providers |

| Prescription coverage (varies) | Same-day or urgent primary care |

| Mental health services (varies) | Low cost after deductible |

Key barriers that insured adults still face include network restrictions that limit your doctor choices, high deductibles that make routine care feel unaffordable, prior authorization requirements that delay care, and limited appointment availability at in-network practices.

Pro Tip: Always confirm your provider is in-network before booking an appointment. One quick phone call to your insurer or a check on the practice’s website can save you from an unexpected bill.

How insurance design impacts your costs and choices

Your plan type shapes almost every aspect of your healthcare experience. In New Jersey, the three most common plan types for adults seeking primary care are HMOs, PPOs, and Medicaid Managed Care plans. Each one operates differently when it comes to seeing a primary care provider, getting referrals, and managing costs.

An HMO (Health Maintenance Organization) requires you to choose a primary care physician (PCP) who coordinates all your care. If you need to see a specialist, your PCP must refer you. This design keeps costs lower but limits your flexibility. A PPO (Preferred Provider Organization) gives you more freedom. You can see specialists without a referral and visit out-of-network providers, though at a higher cost. Medicaid Managed Care in New Jersey operates under state guidelines, with specific rules for PCP assignment, referrals, and coverage.

GetCoveredNJ resources explain that insurance plan type directly determines how you pay for care, which network rules apply, and what prior authorization or referral steps are required.

| Plan type | PCP required | Referrals needed | Out-of-pocket costs | Flexibility |

|---|---|---|---|---|

| HMO | Yes | Yes | Lower | Limited |

| PPO | No | No | Higher | High |

| Medicaid Managed Care | Yes (assigned) | Often yes | Very low/subsidized | Limited |

Here is how to estimate your real annual costs before choosing or using a plan:

- Add up your monthly premiums for the full year.

- Check your plan’s deductible and estimate how quickly you reach it based on your typical care needs.

- Calculate expected copays for primary care visits and any specialist visits you anticipate.

- Review your coinsurance percentage for services after your deductible.

- Compare your total estimate to the plan’s annual out-of-pocket maximum to gauge your worst-case scenario.

Our medical services guide for North Bergen and Secaucus can help you understand what services you might use most often, making this cost estimation process easier. You can also review insurance plan details to confirm your specific plan is accepted before you commit to care.

The big picture: Primary care spending and policy in New Jersey

How much New Jersey invests in primary care at the state level has a real impact on your ability to find timely, quality care as an insured adult. The truth is, New Jersey has historically underinvested in primary care compared to national averages, and that affects wait times, provider availability, and the range of services accessible to patients.

According to a NJ policy analysis from the New Jersey Department of Health, NJ underinvests in primary care with payment rates that fall below national averages. This means fewer providers are incentivized to practice primary care in the state, which reduces your choices and can extend appointment wait times.

Key insight: When primary care payment rates lag behind national benchmarks, providers may limit the number of Medicaid patients they accept, creating access gaps for the very adults who rely on public insurance for their care.

Some of the most pressing policy challenges that affect your access as a patient include primary care workforce shortages in certain regions of New Jersey, payment gaps between what Medicaid reimburses and what private insurers pay, the ongoing need for payment parity so Medicaid patients receive care on equal terms, and limited state investment in preventive care infrastructure.

For Medicaid enrollees specifically, payment parity means that primary care providers receive the same reimbursement rates whether a patient is on Medicaid or private insurance. When parity is not fully implemented, some practices stop accepting Medicaid, which narrows your options.

Learning how to access preventive health services in your area is one practical way to work within these systemic limits. Understanding your primary care options across North Bergen and Secaucus also helps you plan ahead rather than scramble when care is needed.

Insurance literacy: Why understanding your plan matters as much as having one

Having insurance without understanding it is a bit like having a key but not knowing which door it opens. Insurance literacy, meaning your ability to understand your plan’s coverage, rules, and costs, is just as important as enrollment itself.

Research on insurance literacy initiatives shows that low insurance literacy is linked to inefficient care use, delayed primary care visits, and a higher likelihood of using the emergency department for issues that could have been handled at a primary care office. Emergency visits cost far more and are often less effective for managing ongoing health concerns.

Common mistakes that stem from low insurance literacy include assuming all care is covered at the same cost, using out-of-network providers without realizing the financial impact, skipping referral steps required by an HMO and then facing denied claims, missing out on free preventive services because they were unaware coverage existed, and waiting until a health issue is urgent because they thought a visit would be unaffordable.

Understanding what counts as preventive care under your plan is especially valuable. Many screenings, vaccinations, and annual physicals are covered at no cost under the Affordable Care Act, but only when billed correctly and when you see an in-network provider. Learning this distinction can save you hundreds of dollars a year.

A better preventive care workflow starts with knowing what is covered. If you want a clearer picture of how primary care fits into your overall health strategy, our primary care explained resource is a helpful starting point.

Pro Tip: Review your plan’s Summary of Benefits and Coverage document every year during open enrollment. It is a plain-language overview of what your plan covers, what it costs, and what limitations apply. Most insurers make it available online.

In New Jersey, certified enrollment assisters and Federally Qualified Health Centers can also provide free help choosing or understanding your plan.

A critical view: When insurance design creates barriers instead of solutions

Not all insurance design problems stem from underinvestment. Some come from the structure of plans themselves. High-deductible health plans (HDHPs) are increasingly common, and while they lower monthly premiums, they place significant financial risk on you before coverage kicks in. For many adults in New Jersey, this leads to a painful decision: delay or skip primary care to avoid a bill they cannot yet afford.

Worth noting: As one opinion on health insurance reform points out, high deductibles and design flaws in insurance plans can actually raise overall costs and reduce the very protection that coverage is supposed to provide.

Three specific ways insurance design can increase your risk or complexity as a patient:

- High deductibles delay care. When you owe the first $1,500 or more before insurance contributes, a routine primary care visit feels like a financial burden, even when it would prevent a more expensive health event later.

- Complex billing creates confusion. Explanation of benefits forms, balance billing from out-of-network providers, and surprise charges make it difficult to plan financially or understand what you actually owe.

- Prior authorization slows treatment. Many plans require advance approval for certain tests, referrals, or medications. Delays in that process can push back necessary care by days or even weeks.

Knowing the difference between what qualifies as urgent vs primary care helps you make smarter decisions about when and where to seek care, which can also protect you from high costs associated with unnecessary urgent care or emergency visits.

Even if you are fully insured, reviewing your plan’s out-of-pocket risk each year is a responsible step. The goal is to never be surprised by a bill that could have been anticipated.

Our perspective: What New Jersey adults need to know about insurance and primary care

After working with patients across North Bergen and Secaucus, we have seen one pattern repeat itself: people overestimate what their insurance card guarantees. They enroll, assume coverage means access, and then feel blindsided when they hit a deductible, face a referral delay, or discover their doctor left the network.

The most effective patients we see are the ones who treat insurance as a starting point, not a finish line. They confirm that their PCP is in-network before the first visit. They understand their deductible and plan around it. They ask about referral rules before seeing a specialist. And they take a few minutes each year to review their insurance coverage tips so nothing comes as a surprise.

Pro Tip: Think of your insurance card as an entry point. The real work is learning the hurdles your specific plan places between you and care, and then navigating around them with confidence.

Knowledge is just as important as coverage. Both together give you the best chance at timely, affordable, high-quality primary care in New Jersey.

Connect with trusted primary care in New Jersey

Understanding your insurance is only part of the picture. Finding a practice that accepts your plan and offers the care you need is the other half.

At Garden State Medical Group, we have built our practice around making primary care accessible to insured adults in North Bergen and Secaucus. We accept a wide range of plans and work to make the process of using your insurance as straightforward as possible. Whether you are managing a chronic condition, looking for preventive care, or simply establishing care with a trusted provider, we are here to help. Explore our NJ primary care services, review the insurance plans accepted at our locations, or browse our specialty health programs to find the right fit for your needs.

Frequently asked questions

Does having insurance guarantee I can see a primary care doctor in New Jersey?

No. Even with active coverage, plan network restrictions, appointment availability, and out-of-pocket costs can still limit your real access to primary care. As Rutgers Policy Lab notes, coverage alone does not guarantee you can afford care, find a provider, or get a timely appointment.

What is the difference between HMO, PPO, and Medicaid Managed Care for primary care in NJ?

HMO plans require you to select a PCP and get referrals for specialist visits, PPO plans allow more flexibility without referrals, and Medicaid Managed Care follows specific state rules for PCP assignment and authorizations. GetCoveredNJ outlines how plan type determines referral requirements and PCP rules in New Jersey.

How can I estimate out-of-pocket costs for primary care?

Start by reviewing your plan’s Summary of Benefits and Coverage, confirm your doctor is in-network, then add up your annual premium, deductible, expected copays, and coinsurance. Insurance design shapes every layer of what you ultimately pay for care.

What is insurance literacy and why does it matter?

Insurance literacy is your ability to understand what your plan covers, what it costs, and what rules apply. Low literacy levels in this area are linked to delayed care, inefficient use of benefits, and higher overall healthcare costs.

Is insurance always protective against high healthcare costs?

Not always. High deductibles and restrictive plan designs can leave you with significant expenses even when you are fully enrolled. High deductibles and structure can drive costs higher and reduce the financial protection that coverage is supposed to provide.